Defined Benefit Small Self-Administered Scheme (DBSSAS) Pensions: What are they?

· Posted on: May 5th 2022 · read

For owners of a privately limited company, does this sound familiar?

- Have you not contributed fully to your £40,000 pension annual allowance during the current or latest 3 tax years?

- Do you have a tapered Annual Allowance?

- Do you have a low-level salary and high-level dividends?

- Do you have significant headroom under the Lifetime Allowance?

- Is the company able to make large contributions from either cash or surplus income?

- Does your business have significant levels of retained profits?

- Do you wish to purchase commercial property as an investment or to trade from?

With tax rates increasing and allowances being frozen, owners of their own private limited company may have a reduced ability and willingness to draw income from their company. As such, retained profits can languish in cash deposits, earning little interest against a high inflation backdrop, risking a potential loss of multiple tax allowances or challenges during a business sale.

It feels like a no-win situation ……………. or is it?!

Well, not quite. With a robust financial & tax planning strategy, returns on assets and tax savings can be made.

Contributing to a pension is a familiar action to most, but it is digging deeper into defined benefit or defined contribution arrangements which can broaden planning potential.

Defined Contribution (DC) pensions are predominantly personal pensions, SIPPs and SSASs and these are the most common pensions with self-employed individuals or individuals in the private sector. Defined Benefit (DB) pensions are still prevalent in the public sector, but this style of pension is not just exclusive to the NHS or Fire Service…

Cue the Defined Benefit SSAS (DBSSAS).

A DBSSAS benefits from the same features as a Defined Contribution SSAS (DCSSAS), however, the primary differences are how the final pension is calculated and how contributions are funded and assessed for the purpose of an individual’s Annual Allowance (AA). This means that there is potentially significantly greater scope for the company to contribute to a DBSSAS, than there would be to a DC scheme.

DC pensions receive contributions either gross or net of tax. The limit for tax relief (AA) is generally £40,000 pa (this may be reduced for certain individuals).

The contribution to DB pensions on the other hand, is calculated by accounting for the increase in benefits during the pension year. Let’s assume a DB pension provides an income for an individual of £2,500 pa. HMRC multiply this by 16 to determine how much of the AA has been used.

| DCSSAS | DBSSAS | |

| Method of Annual Allowance assessment | Contributions received | Benefit accrual |

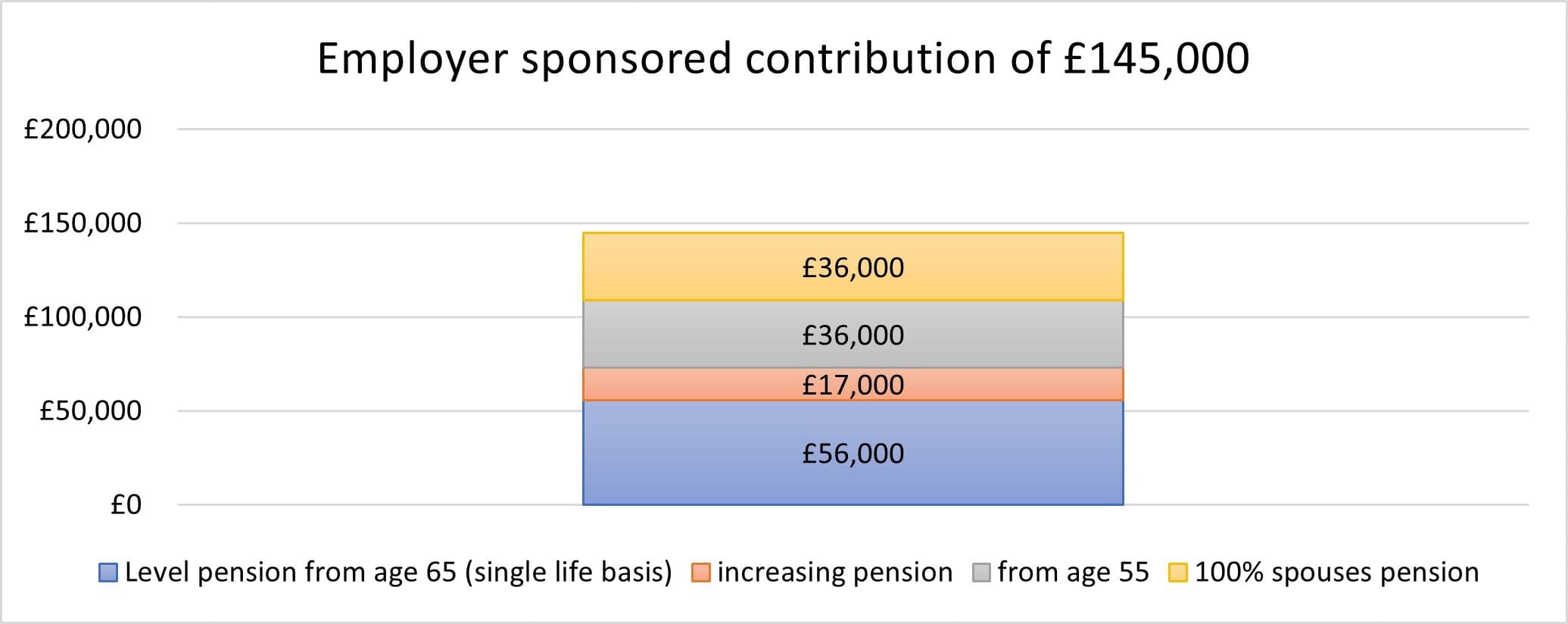

| Maximum annual benefit | Annual Allowance (2022/23) £40,000 | Annual pension of 1/16th of the Annual Allowance £2,500 Cost to an employer to fund (up to £145,000) |

The question therefore is what does a pension like this cost to fund? The answer to this can be “a lot”!

A pension actuary calculates what funds are required to deliver the target income along with other benefits such as inflationary increases, widows’ pensions and other guarantees.

Enhancements to an individual’s benefits are costly, consequently, the contributions actuarially calculated to provide such a pension are considerably greater than the £40,000 as a monetary amount to the sponsoring employer. In principle, here’s how it works:

Values used in the examples in this article are for illustrative purposes only and should not be construed as a personalised recommendation. No action should be taken without seeking further formal advice.

Your personal circumstances and therefore your ability to make use of a DBSSAS pension arrangement, contributions and tax reliefs will vary from individual to individual.

This article should not be construed as a personalised recommendation. The most suitable solution for you will depend on your own personal circumstances. No action should be taken without seeking further formal advice.

MHA Moore and Smalley is the trading name of Moore and Smalley LLP. Moore and Smalley LLP is regulated by the Financial Conduct Authority, FCA registration number 448716.